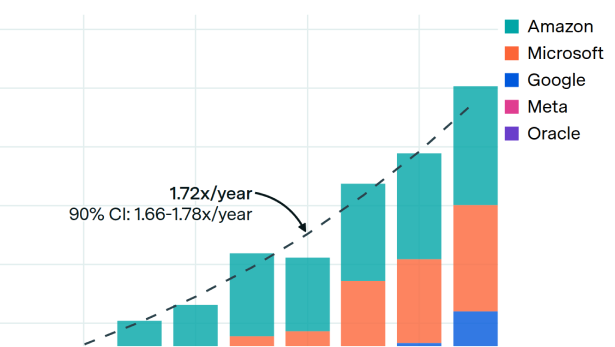

Microsoft acquired $68 billion of physical assets during the second half of 2025, not including replacements for retired goods — nearly as much as the entire prior year. Their financial filings suggest that acquisitions were dominated by spending on new data centers. IT equipment, including GPUs and servers, contributed 57% of the growth, while buildings made up 39%.

Note that gross asset growth is typically lower than total capex (which includes equipment replacement) and higher than net book value growth (which deducts depreciation).

Epoch's work is free to use, distribute, and reproduce provided the source and authors are credited under the Creative Commons BY license.

Learn more about this graph

Microsoft is one of the leading AI “hyperscalers” and the primary compute provider for OpenAI. We analyze changes in Microsoft’s total capital assets using their reports of gross property and equipment (PP&E) disclosed in their SEC filings. We focus on Microsoft because Microsoft and Meta are the only hyperscalers to provide this data on a quarterly rather than annual cadence, and as a cloud compute provider Microsoft is more representative of the group.